Organizational stress and resilience in the arts in Canada

This is the first statistical report in the new SIA Brief series, designed to offer insights into topics such as public engagement in the arts, the wellbeing of artists and arts organizations, and the impacts of the COVID-19 pandemic.

Using recent information from a range of Canadian sources, this report examines organizational stress and resilience in the arts sector. Where available, specific data on the arts and the broader culture sector[1] are provided. However, because such data are limited, this report also includes recent data related to the “arts, entertainment, and recreation” industry, the closest approximation of the arts in many published datasets.[2] Canada-wide data are analyzed, because provincial and territorial culture statistics are not yet available for the pandemic timeframe. Most datasets relate to the 2020 calendar year, but others provide information as recent as September 2021. Where possible, pre-pandemic comparisons are also provided, with some data available back to 2006.

Key findings

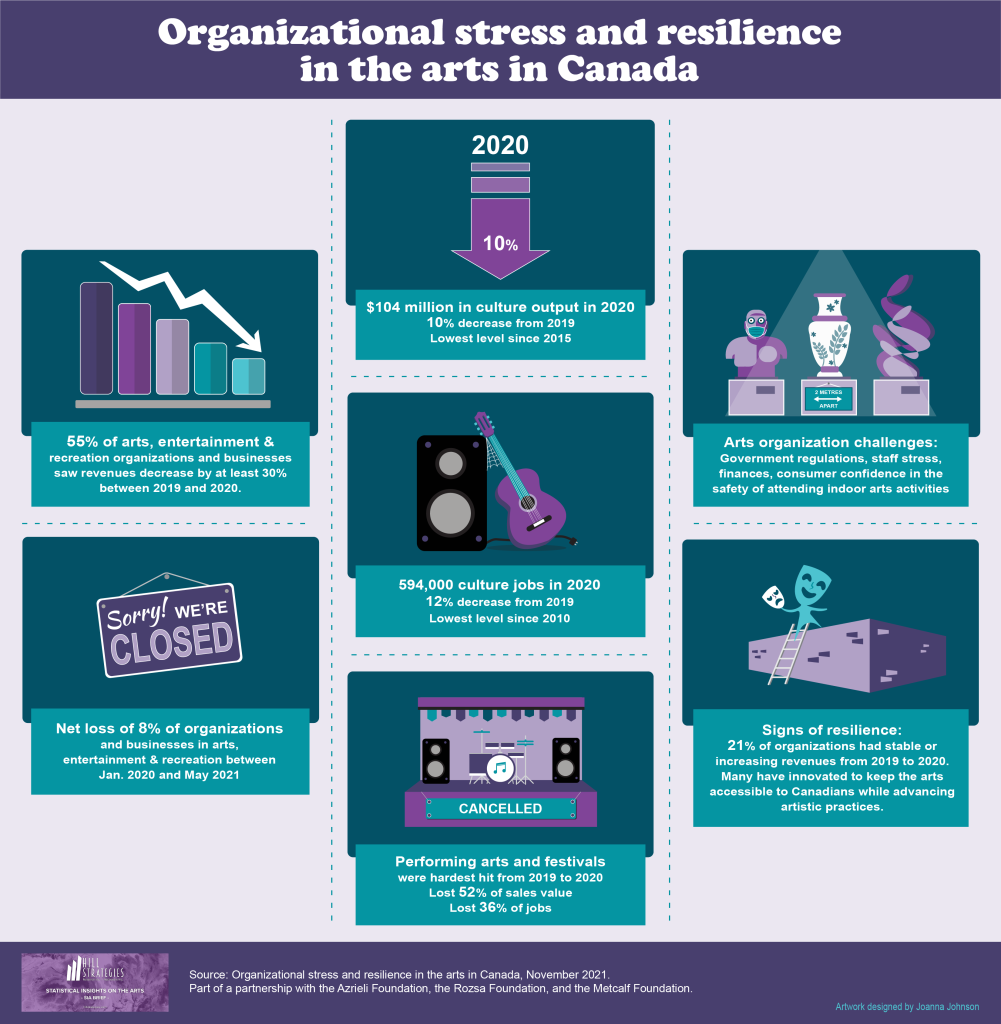

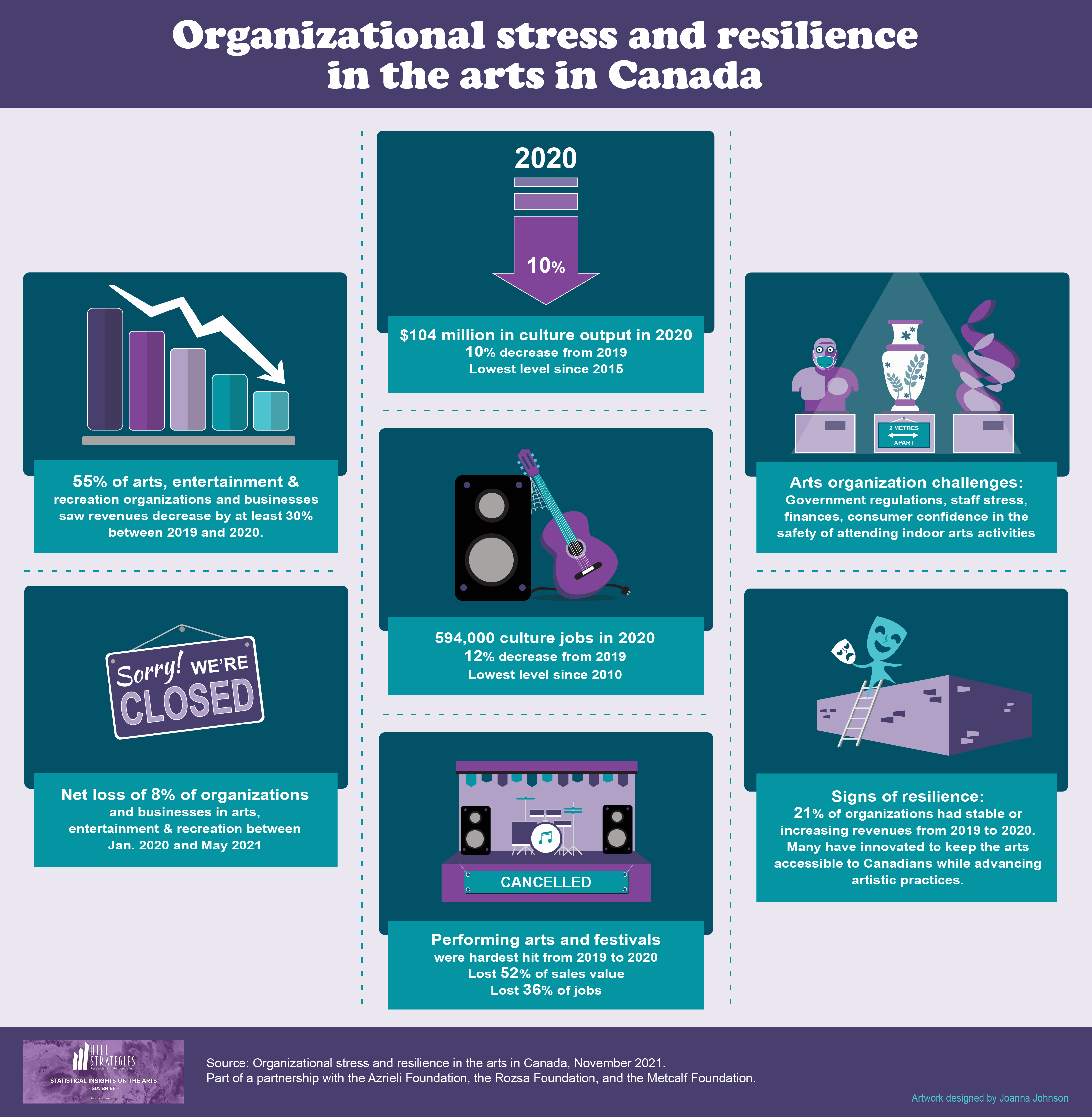

- The total value of all goods and services sold in the culture sector decreased by 10% between 2019 and 2020, reaching its lowest level since 2015.

- Between 2019 and 2020, 55% of organizations and businesses in the arts, entertainment, and recreation experienced a revenue decrease of at least 30% (and 36% experienced at least a 50% decrease). This significant drop in revenue, combined with other factors identified in this brief, has left many organizations in a fragile state.

- Some organizations have closed. In fact, there were 8% fewer organizations and businesses in the arts, entertainment, and recreation in May 2021 than in January 2020.

- The 594,000 employment and self-employment positions in the culture sector in 2020 represented the lowest jobs total since culture specific records began in 2010.

- The performing arts and festivals have been the hardest hit area of the culture sector, losing 52% of sales and 36% of jobs between 2019 and 2020.

- Arts organizations face a range of challenges to their business continuity related to government regulations, staff stress or burnout, financial constraints, and consumer confidence in the safety of attending indoor arts activities.

- Despite these challenges, there is quantitative and qualitative evidence of the resilience of arts organizations.

These key findings point to a unique and challenging financial and work environment for arts organizations in Canada. To overcome their challenges, given that most arts organizations have varied income sources, they require financial support from many different groups: individuals (through ticket sales and donations); governments (through grants and pandemic specific funding); foundations (through grants and pandemic related funding), and businesses (through sponsorships and in-kind support).

On the public health front, many arts organizations are looking forward to a time when it will be safe to have limited or no rules regarding gatherings and seating capacity. In some provinces and territories, this is already the case. However, public confidence in the safety of returning to indoor spaces is also crucial.

Culture sector: lower sales value in 2020 than any year since 2015

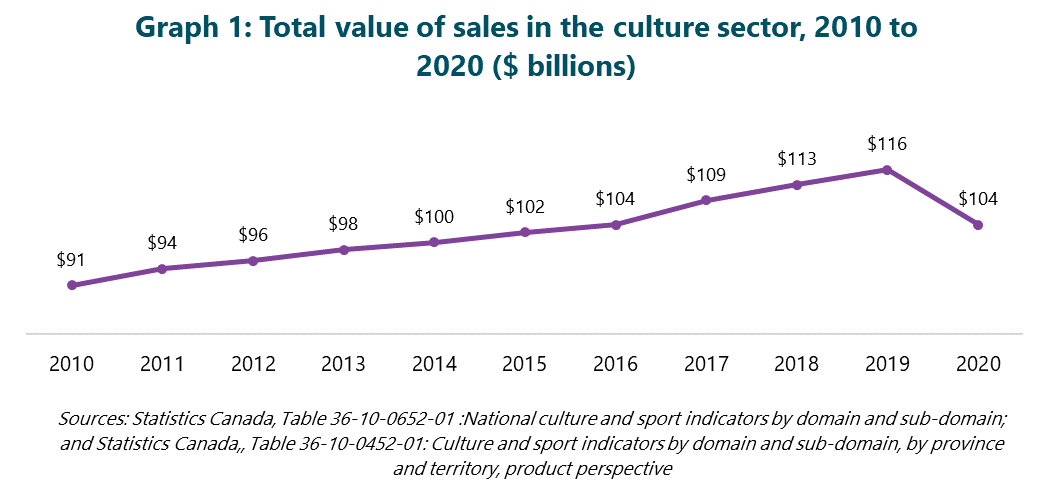

In 2020, the total value of all goods and services sold in the culture sector was just under $104 billion. The sales statistics include, for example, books and e-books, architectural and design services, broadcasting, works of art, as well as admissions to museums, performing arts events, and movie theatres. The statistics also include an imputed value (at cost) for culture goods and services that are offered for free.[3]

Graph 1 shows that the 2020 level ($104 billion) was a 10% decrease from 2019 ($116 billion) and just below the level in 2016 (which also rounds to $104 billion).[4] Not-for-profit organizations, businesses, and artists in the performing arts and festivals collectively lost 52% in sales between 2019 and 2020, the largest loss of any culture domain. (None of the statistics in this report have been adjusted for inflation.)

An important factor contributing to the sales decrease is a reduction in household spending on culture during the pandemic. Spending on “recreation and culture services” decreased by 18% between 2019 and 2020, reaching its lowest level since 2006.[5]

Note: Above graph and data corrected to “$ billions” (from “$ millions”). Unfortunately, Statistics Canada’s tables do not indicate that figures are expressed in “thousands of dollars” rather than just “dollars”.

Many vulnerable organizations

As noted in our recent blog post, there was an 8% decrease in the number of active organizations and businesses with at least one employee in the arts, entertainment, and recreation sector between January 2020 and May 2021. This decrease was much larger than the average decline in all sectors of the economy (-1%).[6]

Many organizations and businesses that did not close or become inactive are in a fragile state. Between 2019 and 2020, more than one-half of organizations and businesses in the arts, entertainment, and recreation experienced a revenue decrease of at least 30%. The 55% of organizations and businesses in this situation include the 36% that lost at least one-half of their revenues.[7]

In January 2021, the TD Bank published a Business Vulnerability Index by Industry, which incorporated survey data on organizations’ revenue decreases, risk of closure, debt, and cash on hand.[8] At that time, the vulnerability index was highest for organizations and businesses in the arts, entertainment, and recreation sector, higher even than the accommodation and food sector. Using more recent data (from the third quarter of 2021), the accommodation and food sector had surpassed the arts, entertainment, and recreation sector on this measure of vulnerability. As shown in Graph 2, these two sectors rank highest on this index. There is slightly above average vulnerability in the information and cultural industries sector, which includes publishing, motion pictures, sound recording, and broadcasting, along with software, telecommunications, and data processing and hosting.

Arts attendees appear to be quite aware of the fragile state of arts organizations. In an August 2021 survey, 70% of pre-pandemic arts attendees indicated that they are at least somewhat concerned “about the survival of arts/cultural organizations”.[9]

Fewer jobs in culture in 2020 than any year in the 2010s

The total number of employed and self-employed positions in the culture sector decreased by 12% between 2019 and 2020. Graph 3 shows that the 594,000 positions in 2020 represent the lowest level since 2010, when culture specific records started to be kept.[10] In comparison, there were 673,000 jobs in culture in 2019. Performing arts and festivals suffered the greatest job loss of any area of the culture sector, with 36% fewer jobs in 2020 than in 2019.

Challenges in moving forward

In the current environment, arts organizations face a range of challenges in moving forward. About one-half or more of the organizations responding to the National Arts and Culture Impact Survey[11] in late 2020 reported challenges related to:

- Government regulations related to public health orders

- Uncertainty of government actions hindering effective planning

- Staff stress or burnout

- Financial constraints

- Fluctuations in demand for services

- Lack of capacity to adapt to the current reality

- Shortage or inability to access space or equipment

Regarding staff stress levels, 79% of arts organizations responding to the same survey indicated that they were experiencing high or very high levels of stress and anxiety in late 2020, compared with 25% who reported such levels before the pandemic.[12]

At the same time, many arts organizations are facing challenges in hiring staff as they re-open. In the arts, entertainment, and recreation, the vacancy rate for payroll employees was 8.4% in the second quarter of 2021, more than double the rate in the first quarter (3.7%). The 8.4% vacancy rate is the highest since comparable records started in 2015.[13]

Another significant challenge is the hesitancy of many Canadians to return to arts activities, even if other attendees are fully vaccinated. A national survey in August 2021 showed that over one-half (56%) of pre-pandemic attendees expected to wait before they return to indoor arts or cultural performances, the largest proportion of whom (31% of attendees) were unsure when they would return. The survey results were similar regarding visiting art galleries and museums, where 49% of pre-pandemic arts attendees expected to wait before they return, including 31% who were not sure when they would return.[14] With the shifting and varied state of the pandemic across Canada, it is difficult to accurately gauge consumer confidence in the safety of attending indoor arts activities.

Signs of resilience

One positive economic sign is the fact that the total value of all goods and services sold in the culture sector was 16% higher in the second quarter of 2021 than the same quarter of 2020 (the first full quarter influenced by the pandemic). In fact, after a sharp pandemic induced decline in the second quarter of 2020, sales in the culture sector have increased in every subsequent quarter, but they remained 6% lower in the second quarter of 2021 than the quarterly average in 2019.

A detailed breakdown of sales data shows that interactive media was the one area within the culture sector to see an increase between 2019 and 2020 (+2%).

Another positive economic indicator is the fact that, between 2019 and 2020, one in every five organizations or businesses within the arts, entertainment, and recreation (21%) had stable or increasing revenues.

During the pandemic, many organizations have used digital technologies and other creative ways to connect with Canadians, advance their artistic practices, alleviate their financial pressures, and limit staff layoffs and reductions in hours.[15] For example, among arts organizations responding to the National Arts and Culture Impact Survey:[16]

- 82% indicated that they are interested in or already exploring digital opportunities

- 62% offered digital programming between August and October 2020

Qualitative evidence is emerging about resilience among arts organizations. For example, a research project from the Creative City Network of Canada, which will inform future training programs, has gathered stories of resilience from the arts community. Some examples from this new research:[17]

- The Newfoundland Symphony Orchestra, through its new Pay-It-Forward Subscriptions and Seniors Outreach, sustained its concert offering at previous levels, generated new revenue streams, and virtually reached audiences in remote parts of Newfoundland and Labrador where the orchestra had never toured before.

- rice & beans theatre, a small company based in Vancouver, modified a stage play into a digital installation and digital interactive stories. The production (Yellow Objects), which highlights the pro-democracy and social justice movements in Hong Kong, allowed rice & beans to hire many artists and reach an expanded audience, despite the pandemic.

- The Woodland Cultural Centre, a First Nations Educational and Cultural Centre located on the grounds of the former Mohawk Institute Residential School near Brantford (Ontario), is a leader in the revitalization and celebration of Indigenous history, art, language, and culture, particularly those of the Haudenosaunee, Anishinaabe, and Ongwehon:weh. During the pandemic, the Centre pivoted its tours to a virtual format, which proved so popular that they represent a substantial new revenue stream, in addition to their role in building dialogue and raising awareness of Indigenous culture.

- Kiran Ambwani, a Montreal based artist who is a board member at Festival accès Asie, developed a new approach in her photography, involving screen capture and substantial participation by her photographic subjects. By connecting with 135 artists from across Canada, she deepened her networks and gave visibility to Asian artists, which could be one small step in countering the increase in anti-Asian racism during the pandemic.

Limitations

There are some elements that we would have liked to examine if data were available:

- A measurement of organizations’ sales of goods and services (separate from individuals).

- Provincial and territorial data: data for 2020 will be published but were not available in time for this report; quarterly data are not available for the provinces and territories.

- Greater specificity of data for the arts, rather than the “arts, entertainment, and recreation” industry or spending on “recreation and culture services”.

- Recent, aggregate data on attendance at arts organizations as some jurisdictions emerge from the pandemic.

- Information about the stress and resilience of different arts organizations, including those in different disciplines, Indigenous led groups, Black led groups, women led organizations, and more.

Notes

[1] Statistics Canada data related to the “culture sector” include: live performance; visual and applied arts; written and published works; audio-visual and interactive media; sound recording; heritage and libraries; education and training; and governance, funding and professional support.

[2] The three subsectors within this industry group are: 1) performing arts, spectator sports, and related industries; 2) heritage institutions; and 3) amusement, gambling, and recreation industries, https://www23.statcan.gc.ca/imdb/p3VD.pl?Function=getVD&TVD=1181553&CVD=1181554&CPV=71&CST=01012017&CLV=1&MLV=5. This industry group excludes cultural industries (such as publishing, motion pictures, sound recording, and broadcasting), which are grouped into “information and cultural industries”, along with software, telecommunications, and data processing and hosting.

[3] In this report, the term “sales value” equates to Statistics Canada’s term “output”. Statistics Canada’s description of production and output, including the calculation for free items, is available at https://www150.statcan.gc.ca/n1/pub/13-604-m/2015079/appb-annb-eng.htm. The commonly cited measure of Gross Domestic Product is a de-duplicated, value-added indicator, based on total output. Total output provides a useful measure of overall economic activity from artists and cultural organizations.

[4] Not adjusted for inflation. Annual data for 2010 through 2019 from Statistics Canada. Table 36-10-0652-01: National culture and sport indicators by domain and sub-domain, https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610045201. Data for 2020 calculated from quarterly statistics in Table 36-10-0452-01: Culture and sport indicators by domain and sub-domain, by province and territory, product perspective, https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610065201. Because the quarterly statistics for 2020 are not available on a provincial or territorial level, only nationwide culture specific data are included in this report.

[5] Statistics Canada. Table 36-10-0107-01: Household final consumption expenditure, quarterly, Canada, https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610010701.

[6] Kelly Hill, On precarity in the arts, https://hillstrategies.com/2021/10/13/on-precarity-in-the-arts/. The data were analyzed by Hill Strategies Research from raw data in Statistics Canada. Table 33-10-0270-01: Experimental estimates for business openings and closures for Canada, provinces and territories, census metropolitan areas, seasonally adjusted, https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3310027001

[7]. Statistics Canada, Table 33-10-0317-01: Business or organization revenue from 2020 compared with 2019, by business characteristics, https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3310031701&pickMembers%5B0%5D=3.13.

[8] TD’s description is here: https://economics.td.com/ca-assess-stress, Original report based on Statistics Canada, Canadian Survey on Business Conditions, third quarter 2020, https://www150.statcan.gc.ca/n1/daily-quotidien/201113/dq201113a-eng.htm .Updated analysis by Hill Strategies Research based on Statistics Canada, Canadian Survey on Business Conditions, third quarter 2021, https://www150.statcan.gc.ca/n1/daily-quotidien/210827/dq210827b-eng.htm.

[9] Business/Arts, National Arts Centre, and Nanos Inc., Culture goers are concerned about the survival of arts and culture organizations, October 2021, http://www.businessandarts.org/resources/arts-response-tracking-study/.

[10] Sources: Annual data for 2010 through 2019 from Statistics Canada. Table 36-10-0652-01: National culture and sport indicators by domain and sub-domain, https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610045201. Data for 2020 calculated from quarterly statistics in Table 36-10-0452-01: Culture and sport indicators by domain and sub-domain, by province and territory, product perspective, https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3610065201. Because the quarterly statistics for 2020 are not available on a provincial or territorial level, only nationwide culture specific data are included in this report. The jobs estimate prorates part year positions but fully includes part time positions. See https://www150.statcan.gc.ca/n1/pub/13-604-m/2015079/glo-eng.htm.

[11] PRA Inc., National Arts and Culture Impact Survey: Organizations Report, January 2021, https://oc.ca/en/national-arts-and-culture-impact-survey/.. It should be noted that organizations based in Quebec and British Columbia were underrepresented in this survey.

[12] PRA Inc., National Arts and Culture Impact Survey: Organizations Report, January 2021, https://oc.ca/en/national-arts-and-culture-impact-survey/..

[13] Statistics Canada, Table 14-10-0326-01: Job vacancies, payroll employees, job vacancy rate, and average offered hourly wage by industry sector, quarterly, unadjusted for seasonality, https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1410032601.

[14] Business/Arts, National Arts Centre, and Nanos Inc., Culture goers are concerned about the survival of arts and culture organizations, October 2021, http://www.businessandarts.org/resources/arts-response-tracking-study/.

[15] See, for example, Statistics Canada, Financial impacts of the pandemic on the culture, arts, entertainment and recreation industries in 2020, by Marie-Christine Bernard and Megan McMaster, August 2021, https://www150.statcan.gc.ca/n1/pub/45-28-0001/2021001/article/00033-eng.htm

[16] PRA Inc., National Arts and Culture Impact Survey: Organizations Report, January 2021, https://oc.ca/en/national-arts-and-culture-impact-survey/..

[17] Project information and stories of resilience are available at culturalresilience.ca. The research team, led by Kelly Hill of Hill Strategies Research, includes the four researchers who prepared the stories cited here (Blanche Israël, Anju Singh, Melanie Fernandez, and Myriam Benzakour-Durand), plus JP Longboat and Margaret Lam.

{kind=link}